General

More Good Litigation News for the Charitable Sector

07.21.2026 | Linda J. Rosenthal, JD

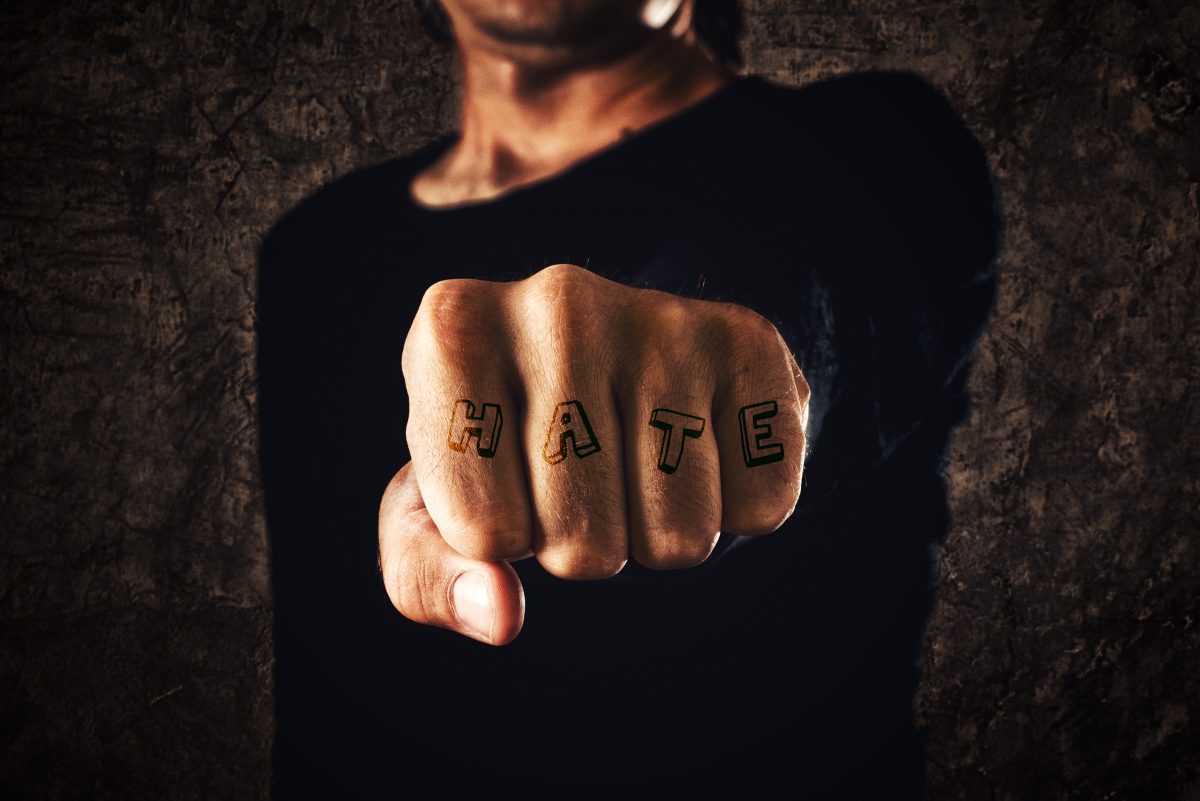

Every few days or so, there’s another hate-group-fueled shooting rampage in the United States. In a long-overdue move, the FBI recently designated the white-supremacy movement as the greatest domestic-terrorism threat of our era.

Along with growing public concern about the rising death toll is a sense of outrage against the extremist organizations that promote and encourage these violent acts. And many of these groups have a federal tax exemption.

The American people have questions: Why do hate groups obtain and keep valuable tax exemptions? The public, along with members of Congress, now want answers.

On September 19, 2019, the House Oversight Subcommittee, in coordination with the Ways and Means (tax-writing) Committee, held a hearing: “How the Tax Code Subsidizes Hate.” The entire hearing, lasting about 2-½ hours, is on YouTube, here. There are also written transcripts; see below.

The answer to this urgent tax exemption issue is as elusive today as it was 2-½ years ago when we posted Can Hate Groups Have 501(c)(3) Educational Status? (February 3, 2017): “The issue is a thorny one for the Internal Revenue Service, which must balance First Amendment rights against concerns that it is essentially granting government subsidies to groups holding views that millions of Americans may find abhorrent.”

It’s been a sticky issue for decades, arising in large part from a tax statute of a single word with no guidance. An organization may qualify for 501(c)(3) status if it is organized and operated exclusively for “educational” purposes. In its entirety, section 501(c)(3) has just 32 words.

Using the customary authority given by Congress to administrative agencies to adopt regulations interpreting statutes, the Treasury and the Internal Revenue Service adopted brief regulations. It was a valiant try, but – (not unlike a product that looks good on an assembly line, only to be exposed as unworkable when it’s launched and tried out in real life) – these regulations just haven’t done the trick.

In the September Congressional hearing, lawmakers “considered whether and how federal tax law could be altered to prevent hate groups from benefiting from tax-exempt status and tax-deductible charitable donations.” Ways and Means Chair Richard Neal’s (D-MA) opening remarks set the tone: “Today’s hearing is a very somber one, but also a very important one. Hate is becoming mainstream in this country,” adding that “groups that propagate white supremacy, anti-Semitism and hatred for the LGBTQ community, among others do not deserve government subsidies through tax exemptions.”

Oversight Subcommittee Chair (the late) John Lewis (D-GA) agreed, noting that the federal tax code “exempts some charitable and educational organizations from paying taxes. Some of these organizations promote hate based on race, gender, religion, sexual orientation, or ethnicity.” He concluded: “Their actions taint the good work of all tax-exempt organizations.”

The top Republican on the House Ways and Means Oversight Subcommittee Mike Kelly (R-PA) concurred: “We can all unite around the belief that racist and discriminatory abuse are repulsive and strongly denounce it. And I understand and share that desire to limit such offensive and disgusting views.“ But Ranking Member Kelly cautioned that there are important First Amendment considerations. “We’re always on a slippery slope when it comes to how we would handle this situation.

The hearing proceeded on two tracks. First, a group of three witnesses, each of whom was connected with a recent mass-shooting incident, gave powerful testimony of the impact on them and their communities of the senseless violence. This evidence reinforced the urgency of action.

Second, two experts on tax-exemption law testified about the pertinent rules and regulations governing decisions to award exempt status. In this part of the hearing, it became clear that despite the unanimity of condemnation of hate groups, withholding a requested tax exemption is no easy matter.

First up in the second track of the hearing was Marcus Owen, Esq., who was a 25-year veteran of the IRS Exempt Organizations Division, including as division director. A link to the transcript of his testimony is here. He is now a partner in a prestigious law firm in Washington, D.C. Next was Professor Eugene Volokh of UCLA Law School, a recognized tax and constitutional law expert. See here for a transcript.

According to a review and critique of this hearing by fellow nonprofit tax law professor, Darryll K. Jones: “Those two legal experts pretty much provided expected, if unimpressive, testimony. Unimpressive only because they both agree that ‘hate speech’ is something we hate, but also something that must be tolerated, and indeed subsidized through tax exemption, because that is the only way to preserve all forms of beneficial speech and debate.” Prof. Jones also offers his opinion that Prof. Volokh “might be best described in this context as a First Amendment purist.” Similarly, in his lengthy commentary in his (paywall-protected) publication, fellow IRS EO Division alum Paul Strekfus has some concerns with the outer boundaries of Volokh’s constitutional analysis.

An important part of Marcus Owens’s presentation is his common-sense observation that even if the government and the courts were to be able to fashion a workable test to determine the definition and application of “educational,” the current state of IRS oversight of charities is dismal. Due, of course, in large part to Congressional hostility and rampant budget-slashing in recent years, the exempt organizations division has been rendered largely impotent.

This has been exacerbated by the disastrous 2014 decision to adopt the streamlined Form 1023-EZ; the so-called “review” process is more like a de facto rubber-stamp approval. While the plan was to pick up problems in a post-approval audit, this has been effectively negated by the fact that just a tiny number of exempt organizations are subject to audit each year.

Mr. Owens calls attention also to a nefarious practice used by some extremist groups to circumvent the tax-exemption application process entirely. These groups find a defunct but not dissolved organization with an existing tax exemption and a nebulous name, and then “revive” it with their own directors, officers, board, and program.

Marcus Owens also discusses an idea that surfaces from time to time; namely, that the federal oversight of charities should be yanked out of its long-time home in the Internal Revenue Service. The duties are diametrically opposed; main IRS tries to optimize the collection of revenue while the exempt organizations division exists to – effectively – give away revenue opportunities. In addition, difficult analyses of tax-exemption qualification – like this one! – involve legal and philosophical concerns not well suited to the more accounting-focused bent of the nation’s tax collection agency.

– Linda J. Rosenthal, J.D., FPLG Information & Research Director

Sign up to be notified when we publish news and articles that impact nonprofits, social entrepreneurs and philanthropists.